Source: Franke et al., "What You Are Is What You Like -- Similarity Bias in

Venture Capitalists' Evaluations of Start-Up Teams" in J. of Bus. Venturing 21 (2006), pp. 802-26

The Context.

In Field Note #131: On "Investment Edge," I attempted to operationalize ways to increase the chances of sustainably capturing investment edges. In the section on "Behavioral Edge," I advanced 5 suggestions for extracting this behavioral risk premium, the "most persistent source of market inefficiency." (n.b. its persistence is suggestive of the difficulty of extraction.)

I failed to account for a sixth--and perhaps most important--suggestion: team diversity. Seemingly mundane, absolutely.

(From my limited vantage point, it appears that internet discourse is optimizing for not boring people, so perhaps my journey into this topic is an accidental rejoinder.)

The Details.

The thesis expounded in the source article is abundantly simple, yet rarely underpinned in my (personal) experience of and in the investment business. And, for better or worse, I have seen and have been directly involved in its wide surface area.

Thesis:

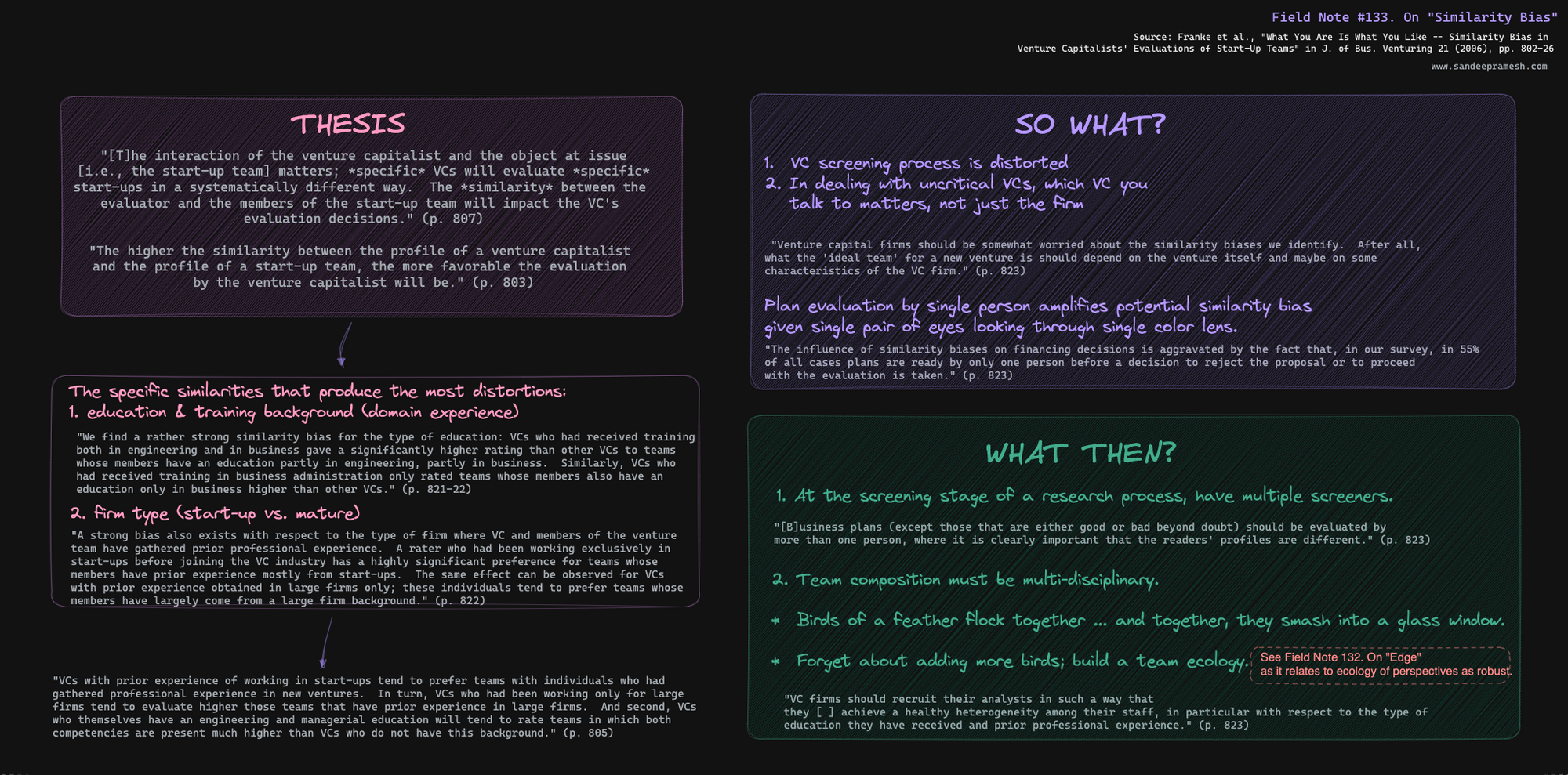

"[S]ystematic distortions of VC evaluations ... derive from the similarity between rater (VC) and ratee (start-up team) .... 'The higher the similarity between the profile of a venture capitalist and the profile of a start-up team, the more favorable the evaluation by the venture capitalist will be.'" (p. 803)

Implication:

The screening process is distorted, especially at the early stages of company development where many VCs focus on management / founding team assessment.

Specifically, (a) education and professional domain experience and (b) organizational structure (startup vs. mature company, e.g.) are the attachment points that create the most evaluative distortions.

Many focus on how to screen and evaluate companies (essential), but gloss over the question of "who" is evaluating. Similarity biases may be a non-trivial contributor to the obscenely common results of the venture business.

Investors tend to overestimate their ability to judge founding teams. The similarity bias is a partial attempt to explain this observation. Add to this the fact that management teams tune their statements to what they think investors want to hear.

The siren song of "pattern recognition" might just turn out to be the cacophony of investment ruin when the notes are really pitched to a negative version of similarity bias. (Aren't the most incredible returns precisely those asymmetries that defy ex-ante pattern recognition?)

Pragmatic Suggestion:

"[B]usiness plans (except those that are either good or bad beyond doubt) should be evaluated by more than one person, where it is clearly important that the readers' profiles are different. This leads to the third suggestion, namely, that VC firms should recruit their analysts in such a way that they [ ] achieve a healthy heterogeneity among their staff, in particular with respect to the type of education they have received and prior professional experience." (p. 823)

While I have left aside methodological issues (e.g., small sample size and questionnaire-based inquiry) with the paper's findings, I took away from the piece a self-reflective moment in considering how, in my own work endeavors, the mantra of "like begets like" can take on such a strong significance that it amputates diverse perspectives needed to surf wildly non-linear waves.

The Mind Map.